Mortgage Blogs

Stay up to date with the recent industry news and mortgage trends.

Capital Gains Tax Changes: Are They Happening or Not

Understanding the Proposed Changes to Canada’s Capital Gains Tax

In June 2024, the Canadian federal government proposed increasing the capital gains inclusion rate—the taxable portion of profits from selling investment properties, secondary homes, or cottages. This change could significantly impact investors and property owners who are thinking about selling.

Currently, 50% of capital gains are taxable. The proposed increase would raise this inclusion rate to 66% or higher, meaning a larger portion of your profits from selling property could be taxed.

As tax expert Jamie Golombek explains in the Financial Post, “Uncertainty remains as to what the final capital gains tax rules will look like, or even if they will be implemented at all.”

Adding to the confusion, the Canada Revenue Agency (CRA) has announced it will begin collecting taxes based on the proposed higher inclusion rate until a final decision is made. Even if the proposal doesn’t pass, you could still face a larger tax bill this year, with possible adjustments later.

Do You Have to Pay Capital Gains Tax if You Sell Your House?

It depends on the type of property you’re selling:

Primary Residence: Typically exempt from capital gains tax under the Principal Residence Exemption (PRE).

Investment or Secondary Property: Profits from selling rental properties, cottages, or vacation homes are taxable and could be hit harder if the inclusion rate rises.

This means that selling an investment property now may not provide the tax advantage some hope for, especially with the CRA applying the proposed rate.

Smarter Alternatives to Selling Your Property

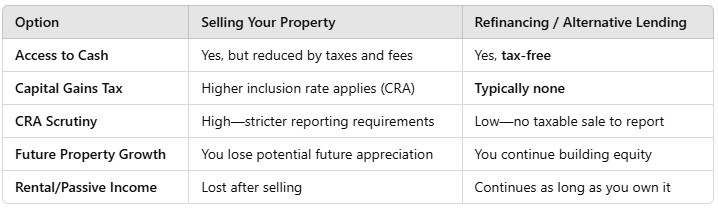

Selling isn’t your only option. If you need access to cash, there are smarter, more tax-efficient ways to tap into your property’s value without triggering a capital gains tax.

Refinance Your Mortgage

Borrow against your home equity for tax-free cash while keeping your property and potential for future growth.

Work with Alternative or Private Lenders

Access quick financing through more flexible lending options when traditional refinancing isn’t ideal.

Consider a Reverse Mortgage (For Canadians 55+)

Unlock tax-free equity without monthly payments and continue living in your home.

Explore No-Payment Loan Options

Interest-only or deferred payment loans can ease financial pressure while preserving long-term assets.

Selling vs. Refinancing: Which Makes More Sense?

Let’s Build a Strategy That Fits Your Goals

Navigating these tax changes can be overwhelming, but you don’t have to figure it out alone. I collaborate directly with your accountant to create a custom strategy that helps you minimize taxes and achieve both your short- and long-term goals.

I offer a clear, side-by-side comparison of your options—whether it’s refinancing, exploring private lending, or considering a reverse mortgage—so you can make the best decision for your financial future.

Know someone else struggling with these decisions? Share this post! Many Canadians don’t realize they have better options than selling.

Let’s talk and figure out what works best for you.

Trusted Guidance, Proven Success

Mike L. - Calgary

Working with Jayden to buy a rental property was seamless and stress-free. Their expertise and support were invaluable. Highly recommend for anyone looking to invest!

Kim W. - Calgary

I had a fantastic experience working with Jayden! As a first-time homebuyer, the guidance provided was clear and supportive, making the process smooth and stress-free. Highly recommended!

James C. - Calgary

When a friend suggested I work with Jayden to renew my mortgage, I was blown away by the experience. Their dedication to find me the best deal in the market was incredible. Thankful I didn't just stick with my bank.

Jayden Backs | Mortgage Broker

(403) 370-9020

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Get In Touch With

(403) 370-9020

Assistance Hours

Mon – Fri 9:00am – 8:00pm

Saturday/Sunday – CLOSED

Contact Us

© 2025 Jayden Backs Mortgage Solutions - All Rights Reserved.

Jayden Backs, Mortgage Broker

BRX Mortgage Inc. RECA